ASM delivered a strong performance yet again in 2022. Sales increased by 33% at constant currencies, despite challenging supply-chain conditions, and a weakening economic outlook in the second half of the year. We made good progress against our strategic targets, continuing to invest in the growth of our business and further expanding our engagements with key customers for new applications.

“Our core values are We Care, We Innovate, We Deliver. They are central to all we do at ASM, and a cornerstone of our culture.”

I want to thank all our people at ASM as they went again the extra mile to meet our customers’ requirements, and contributed to another successful year for our company.

WFE INCREASED AGAIN BUT IMPACTED BY SLOWING END-MARKETS

The semiconductor market began the year with the expectation of continued solid growth, following strong demand in 2021. But momentum slowed down in several segments during the year. The war in Ukraine, rising inflation and interest rates, and a drop in consumer spending started to impact the smartphone and PC markets. This triggered slowing demand and significant inventory corrections in parts of the market. For the full year 2022, the semiconductor market grew by just 5%, down from approximately 25% growth in 2021.

The wafer fab equipment (WFE) market increased by a high single-digit percentage in 2022, but started to slow down in the course of the year. It was impacted by the weakening semiconductor end-markets, combined with persistent supply-chain constraints. Logic/foundry WFE continued to grow in 2022, driven by advanced nodes investments, while memory WFE, particularly impacted by the weakness in PCs and smartphones, dropped.

Strong financial performance

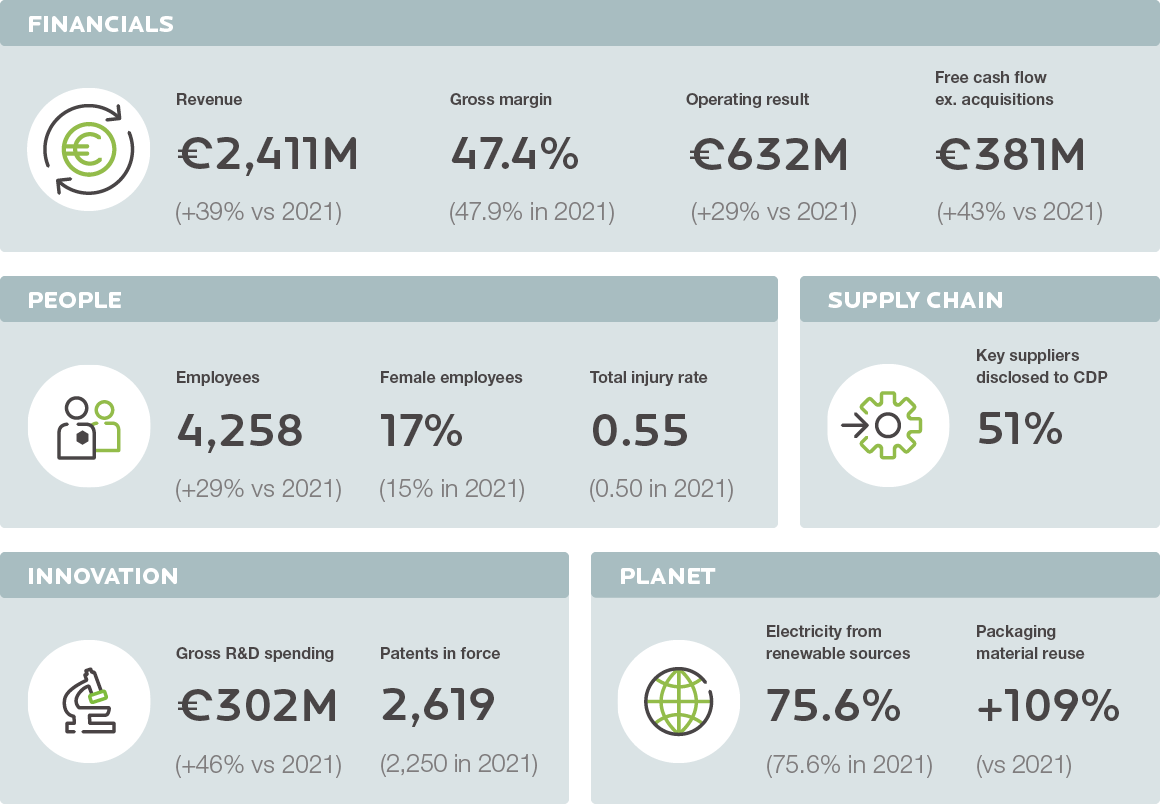

Against this backdrop, our company yet again delivered a very solid performance in 2022. Revenue increased by 33% at constant currencies to a record high of €2.4 billion, our sixth consecutive year of double-digit growth. With equipment revenue growth of 38% at constant currencies — despite difficult supply-chain conditions throughout the year — ASM clearly outperformed the WFE market. Operating profit grew by a solid 29%, even with a substantial increase in operating expenses as we stepped up R&D and further strengthened our organization. Excluding the cash used for acquisitions, free cash flow increased by 43% to €381 million. Our company’s financial position remained strong.

Our ALD business continued to be a key growth driver, accounting for more than half our equipment sales. ALD benefited from solid logic/foundry spending on the most advanced nodes, while we also won important new applications in the memory segment. Epi, our second-largest product line after ALD, was our fastest-growing business in 2022. After announcing our second Intrepid ES customer in 2021, we continued to work towards new customer selections in 2022, expanding our position in the advanced CMOS epitaxy market. In the power, analog and wafer market, we also had solid momentum, supported by our new Intrepid ESA tool for 300mm Epi applications. We believe we’re on track to double our Epi market share from 15% in 2020 to at least 30% by 2025. In vertical furnaces and PECVD, our strategy is to invest selectively. A great example of this is SONORA, our new 300mm vertical furnace platform that we introduced last July. We’ve already booked multiple new wins for SONORA, and expect a solid revenue contribution in 2023.

Acquisitions of Reno and LPE

Another highlight was our two acquisitions in 2022. In March, we announced the acquisition of Reno Sub-Systems, a US-based supplier of RF matching subsystems. Reno’s high-performance RF matching networks and RF generators will enhance our plasma products. In July, we announced the acquisition of LPE, an Italian-based supplier of silicon carbide (SiC) epitaxy systems. SiC is a high-growth market with particularly strong demand in power electronics for electric vehicles (EV), given that it offers higher efficiency, and so extended range or smaller battery size. We expect LPE to generate revenue in excess of €130 million in 2023, up from more than €100 million previously expected. The acquisition of LPE fits perfectly with our strategy and positioning. We expect to drive growth in LPE’s business by leveraging our strong customer base in power electronics. We also aim to further differentiate LPE’s tools on the back of our strengths in areas such as 200mm platform expertise, process chemistries, and cost of ownership. In addition, we see opportunities for synergies in leveraging ASM’s scale and capabilities in areas such as supply-chain management, and our global-service network.

As far as our M&A strategy is concerned, we will continue to scan the market for other acquisition opportunities that could further strengthen our position in the deposition equipment market and drive additional growth.

“THE ACQUISITION OF LPE FITS PERFECTLY WITH OUR STRATEGY AND POSITIONING.”

Growing in all customers segments

Logic/foundry continued to be our largest customer segment. Leading customers continued to invest in advanced node capacity to prepare for the new end-market products that will be introduced in 2023 and beyond. In the newest logic/foundry node, which some of our customers were ramping into high-volume manufacturing by the end of 2022, the number of ALD layers and applications has increased by a strong double-digit percentage. We saw strong traction in R&D engagement and evaluations, especially in ALD and Epi, for the next logic/foundry technology nodes.

Our memory business also delivered solid double-digit growth, driven in particular by 3D-NAND, and despite the slowdown in market conditions in the second half of the year. Demand continued to be strong for ALD high-k metal gate in advanced DRAM devices, in which we believe we have a leading share. In 3D-NAND, we successfully gained a number of new positions for our advanced ALD gap-fill solutions, driving record-high order intake for us in this segment in 2022. At 19% of equipment sales in 2022, memory is still the smaller part of our business. We are working with customers in R&D on several new opportunities, as we remain focused on further strengthening our position in the memory market in coming years.

In the mature node part of the market, we are mainly active in the niche segments of power, analog and wafer manufacturers, with our vertical furnace and part of our epitaxy portfolio. From a smaller base, this part of our business has expanded significantly over the past few years, and is contributing more and more to overall growth for ASM. Next to solid market increases, our growth in the power, analog and wafer segment has been fueled by successful new products, such as Intrepid ESA, and the A400 DUO, our 200mm vertical furnace. With the addition of LPE, we have further strengthened our position in the power segment.

SUCCESSFULLY NAVIGATING CHALLENGING SUPPLY-CHAIN CONDITIONS

A key challenge of the year was the tight supply-chain situation, while at the same time our customers’ demand continued to increase significantly. Supply-chain conditions remained tight throughout the year, particularly in the first three quarters. This resulted in extended lead times and a shortage of materials and components for various parts in our tools, with legacy semiconductors being one of the most critical examples. I’m impressed by our team’s execution and dedication, in close collaboration with our suppliers, in meeting our customers’ requirements. Also, supported by earlier actions such as qualification of additional suppliers and maintaining strategic inventories, we were able to grow our shipments quarter to quarter, and reach record-high sales in 2022.

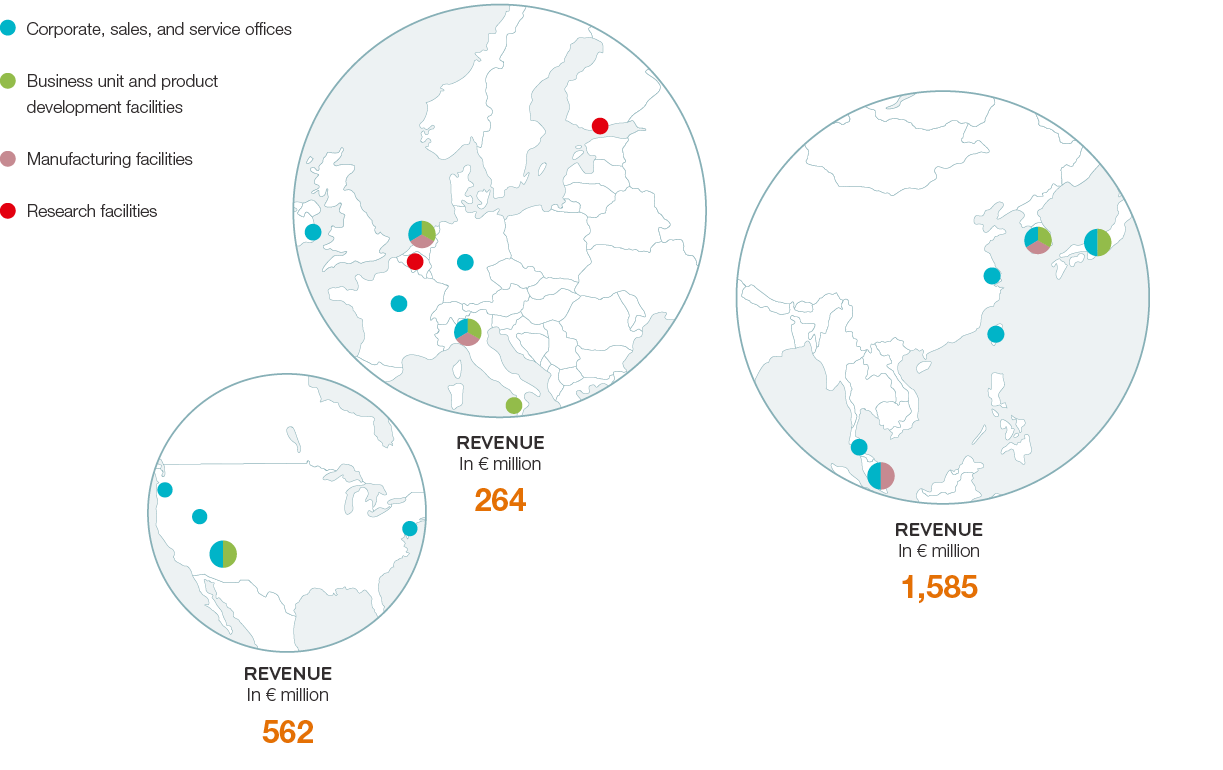

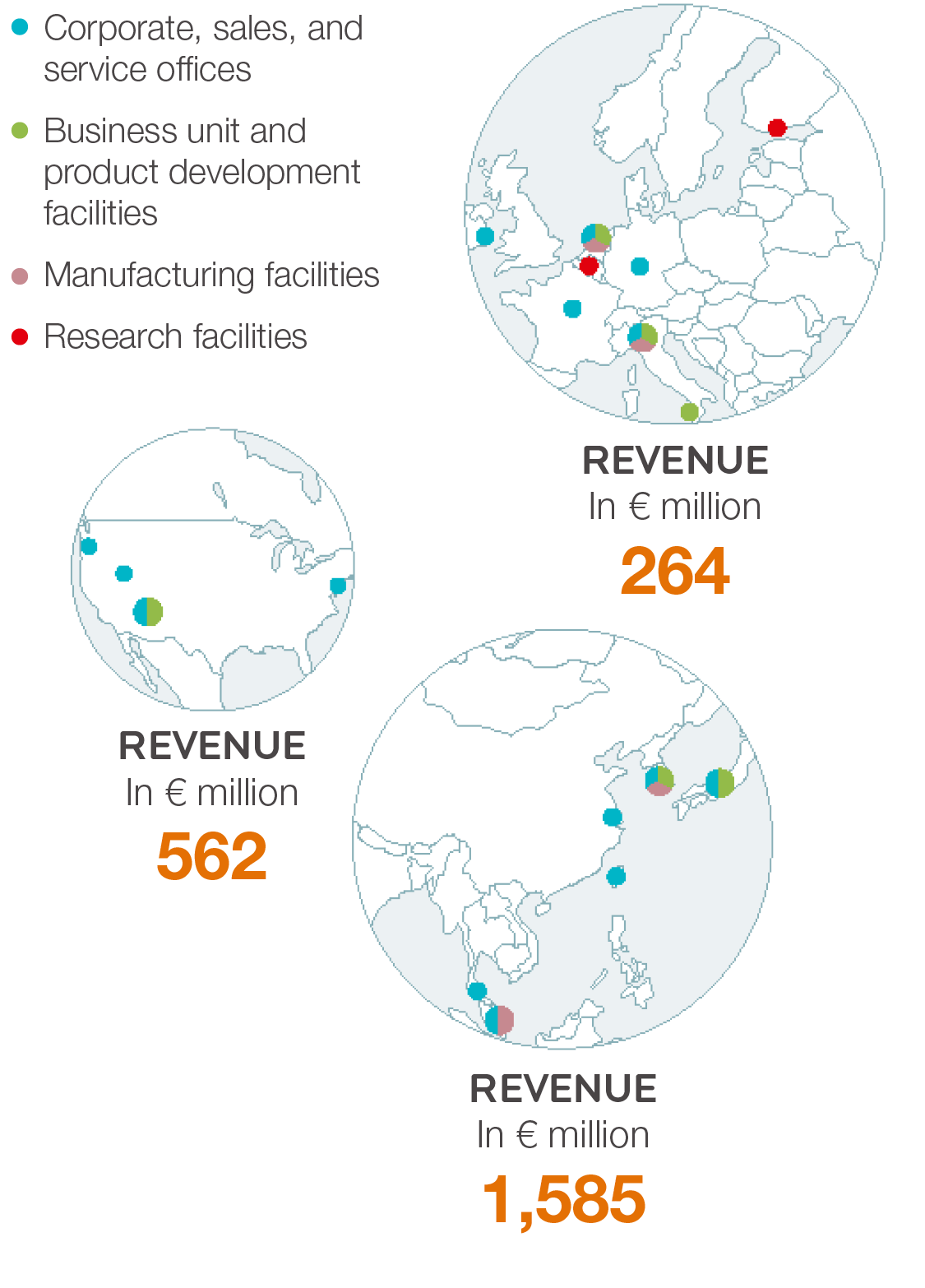

Regarding our own manufacturing capacity, we benefited from timely investments in our new and expanded facility in Singapore, celebrating the official opening in March 2022. Including the second manufacturing floor in this facility, completed in January 2023, we have boosted our global capacity by 3x compared to 2020.

INVESTING IN THE GROWTH OF OUR BUSINESS

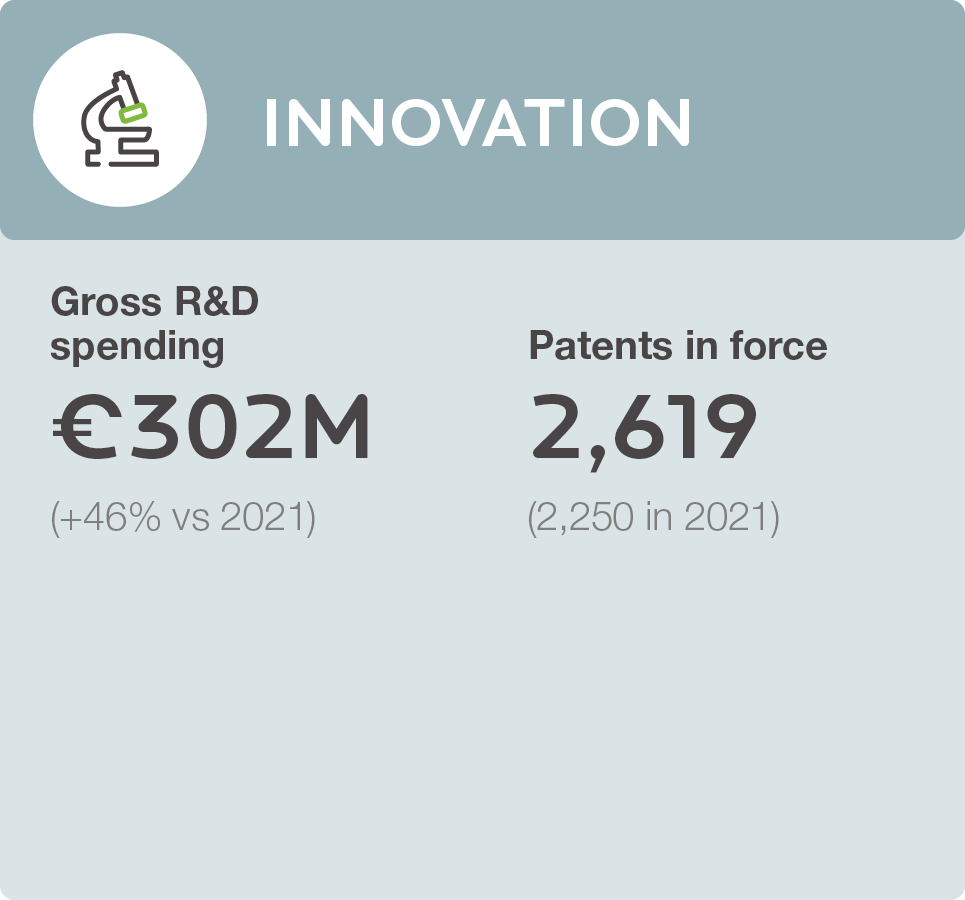

Next to the increase in our manufacturing capacity, we also invested in further upgrading and expanding our R&D facilities. We increased our headcount in R&D by 49%. The number of R&D engagements with customers reached a new record-high in 2022. A key focus in our R&D engagements was the transition in the logic/foundry sector from FinFET to gate-all-around (GAA) device architecture. We expect this transition to result in significant increases in ALD and Epi requirements. As growth opportunities in the mid-term continue to increase, we plan to further increase R&D spending in 2023. In 2022, we also invested in strengthening our organization in many other areas, such as customer field support, IT, supply chain, and HR.

To support growth beyond our mid-term guidance we need to further expand our innovation and manufacturing infrastructure. In February 2023, we announced our intention to significantly increase our R&D and manufacturing facility in Korea. We are also exploring options to expand our activities in Phoenix, Arizona, and in Europe.

PEOPLE ARE OUR BIGGEST ASSET

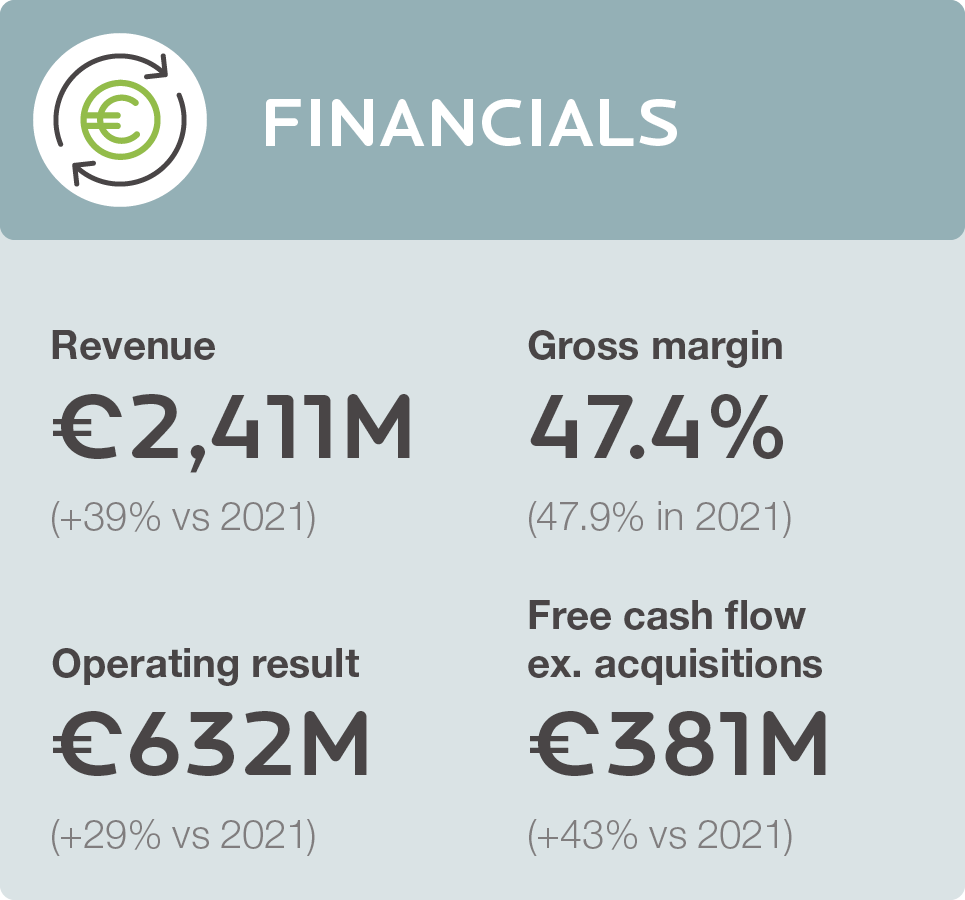

We continue to invest in the growth, engagement, and development of our people. We increased the total headcount by 29% to 4,258 in 2022, despite a continuing tight labor market. I am particularly pleased with the progress on our Diversity & inclusion (D&I) agenda, as the number of female employees increased to 17% of total at the end of 2022, up from 15% in 2021. Our core values are We Care, We Innovate, We Deliver — they are central to all we do at ASM and a cornerstone of our culture. In 2022, we continued to take steps to further embed these values throughout the organization. Safety remains our highest priority. We strengthened our safety culture and contributed meaningfully to the safety of our value-chain partners.

Sustainability highlights

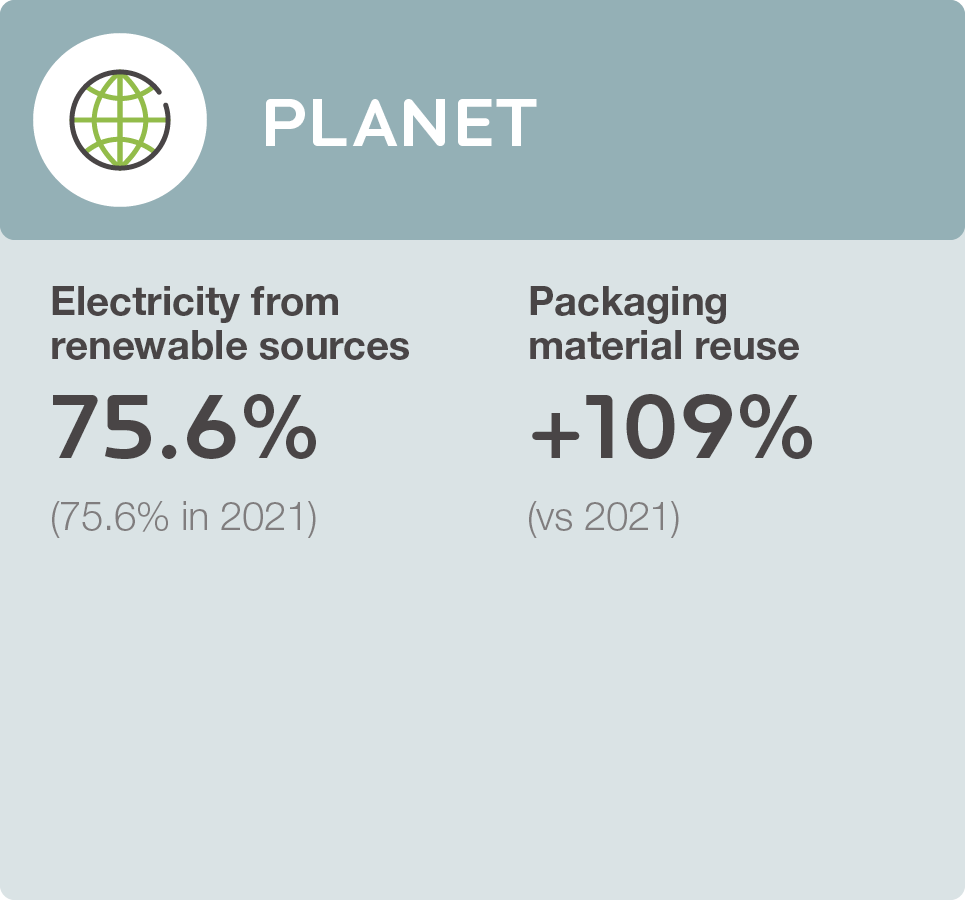

In 2022, we continued our focus on sustainability, one of the key pillars of our strategy. After announcing our Net Zero emissions by 2035 target (all scopes) in September 2021, we took an important next step by submitting our Net Zero measurements and targets for Scope 1, 2, and 3 GHG emissions to the Science Based Targets initiative (SBTi) in December 2022. The SBTi is recognized as the leading body for validation of net-zero targets, and this validation is currently scheduled to start in H2 2023. ASM became a founding member of the new Semiconductor Climate Consortium (SCC), playing a key role in its creation, and ASM has now also been elected as the SCC’s first Chair. One of our key circularity programs is the reuse of packaging. In close coordination with our partners in the value chain, we more than doubled the reuse of shipping materials in 2022. In short, we stepped up our investments in sustainability and have been making great strides in the past few years. It is good to see that our increased focus on sustainability has been reflected in improved ESG ratings, such as with S&P CSA and MSCI, as well as industry accolades.

“IN 2022, WE CONTINUED WITH OUR FOCUS ON SUSTAINABILITY AND TOOK IMPORTANT NEXT STEPS.”

Trade wars and Chips Acts impacting our industry

Several ‘Chips Acts’ were proposed and passed in 2022, such as those in the US, Europe and Japan, as governments around the world work to build and strengthen their domestic chip industries. This reflects the growing importance of semiconductors in our society. Several of our customers have announced plans to expand their overseas manufacturing footprint, a response to their customers’ demand for more geographically diversified supply in view of geopolitical tensions and recent supply-chain disruptions. We expect these investments to start contributing to WFE spending in 2023.

At the same time, geopolitical tensions have triggered new export controls, which negatively impacted the WFE market in 2022. The new US export controls that came into force last October also affected our company. With the 2022 Q3 earnings, we conservatively reduced our backlog with all orders for fabs in the Chinese market that could be impacted by the new export restrictions. And at the end of November, we reported our updated assessment that an expected 15%-25% of our sales in the Chinese market would be negatively impacted. Despite an impact in the fourth quarter, we were still able to book solid growth in our equipment sales from China in 2022, which accounted for 16% of our total sales in 2022. This growth was mainly driven by the mature node segments of power, analog and wafer manufacturers in China, which have not been meaningfully impacted by the recent changes in export controls.

Outlook 2023

Looking at 2023, the global semiconductor market is forecast to contract by some 5% with continued inventory corrections in the first half of the year and a reduced economic outlook. Looking at WFE, logic/foundry spending on the most advanced nodes and automotive-related power/analog demand is expected to remain resilient in 2023. The reduction in memory spending is expected to continue in 2023, while demand for trailing-edge nodes in logic/foundry, especially consumer related, is expected to soften. In total, the WFE market is forecasted to drop by a mid-to-high teens percentage in 2023, a level that we expect to outperform, supported by our strong positions in the leading-edge logic/foundry market, and also by the momentum of newly introduced product and applications. ASM started 2023 with a record-high order backlog of €1.7 billion. On a currency comparable level, we expect revenue for Q1 of €660-700 million, with a slight increase in Q2 revenue compared to this level. Based on the current visibility, we expect revenue in the second half of 2023 to remain at a healthy level, albeit somewhat lower than in the first half of 2023.

“THE NUMBER OF R&D ENGAGEMENTS WITH CUSTOMERS REACHED A NEW RECORD-HIGH IN 2022.”

Long-term prospects continue to be bright

Looking at the longer term, we believe the prospects for ASM continue to be bright. Despite the slowdown in 2023, the structural drivers for our industry are still very much intact. Third-party research firms continue to expect the semiconductor market to grow to more than $1 trillion by the early 2030s. Semiconductors have become essential in all aspects of life, and help to create new applications such as in cloud computing, artificial intelligence (AI), and the electrification of cars. Our customers continue to invest in the development of faster and more power-efficient next-generation semiconductors. These will require further scaling, new device architectures such as GAA, and the introduction of new materials — all of which will drive further demand for our advanced deposition technologies, in particular ALD and Epi. We believe ASM is well positioned to deliver a continued healthy performance.

March 2, 2023

Benjamin Loh

President and Chief Executive Officer

Read less